IATA’s latest figures expose a deeper problem: sustainable aviation fuel needs financeable supply chains, not only additional refinery capacity

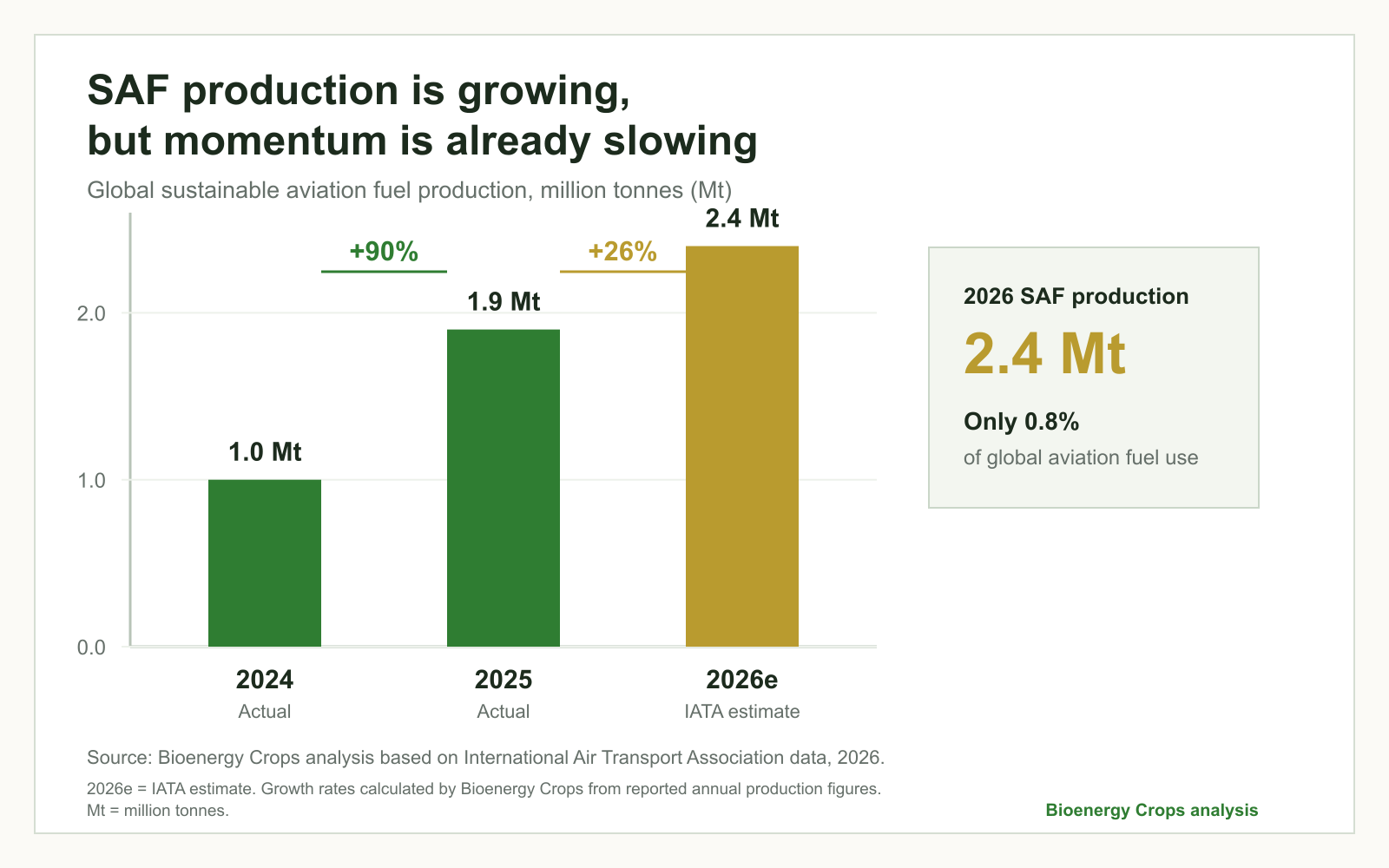

Global Sustainable Aviation Fuel (SAF) production is expected to reach approximately 2.4 million tonnes in 2026, according to the International Air Transport Association. This would represent only 0.8% of total aviation fuel consumption, despite imposing an estimated additional cost of USD 4.3 billion on airlines.

Production roughly doubled between 2024 and 2025, but its rate of expansion is now slowing. The International Energy Agency expects sustainable aviation fuel consumption to rise from around one billion litres in 2024 to nine billion litres by 2030. Even then, it would satisfy only approximately 2% of global aviation fuel demand under the agency’s main forecast.

The figures reveal an uncomfortable gap between policy ambition, announced projects and fuels physically reaching the market.

2026e = IATA estimate. Growth rates calculated by Bioenergy Crops from the reported annual production figures. Mt = million tonnes.

| Year | Production | Status |

|---|---|---|

| 2024 | 1.0 million tonnes | Actual |

| 2025 | 1.9 million tonnes | Actual |

| 2026 | 2.4 million tonnes | IATA estimate |

The International Energy Agency expects global SAF consumption to rise from approximately 1 billion litres in 2024 to 9 billion litres in 2030. Even at that level, SAF would meet only around 2% of global aviation fuel demand under the agency’s main case. Source: International Energy Agency, Renewables 2025.

IATA attributes the disappointing progress to inadequate production incentives, poorly sequenced mandates, insufficient renewable energy, infrastructure constraints and limited participation by major oil companies. These are important factors. However, another structural constraint receives much less attention:

The industry is attempting to build fuel production capacity faster than it is developing the feedstock systems needed to operate that capacity reliably.

A refinery can be technically ready and still remain commercially exposed if its feedstock is expensive, seasonal, dispersed, contested by other industries or insufficiently documented. Sustainable aviation fuel will therefore not scale through refinery investment alone. It requires procurement, agronomy, logistics, storage, certification and risk management to be designed as one integrated industrial system.

Production is growing—but not at the rate required

Sustainable aviation fuel, commonly referred to as SAF, includes renewable or waste-derived aviation fuels that meet applicable technical and sustainability criteria.

Its strategic importance is clear. Aviation cannot easily electrify long-distance operations, while hydrogen-powered aircraft are unlikely to replace most of the existing global fleet in the near term. SAF is consequently expected to deliver a substantial proportion of the sector’s emissions reductions through 2050.

But the scale of the required transformation is often underestimated.

Moving from less than 1% of current aviation fuel consumption to a meaningful share of the market is not a conventional capacity expansion. It requires the creation of a new global system connecting biological resources, renewable electricity, industrial conversion, fuel certification, blending terminals and airports.

The International Civil Aviation Organization tracks a substantial pipeline of announced SAF projects. Announced capacity, however, should not be confused with operating production. Projects must still secure finance, complete engineering, obtain permits, construct facilities, qualify fuels and establish the commercial arrangements required to run at high utilisation rates.

The same distinction applies upstream:

A project announcement is not fuel production, and a resource assessment is not a feedstock contract.

The first generation of SAF supply is highly concentrated

Most near-term production is expected to rely on Hydroprocessed Esters and Fatty Acids (HEFA), known as the HEFA pathway. This technology converts fats, oils and greases into renewable fuels and is currently the most commercially mature SAF route.

Common inputs include used cooking oil, animal fats, vegetable oils and certain industrial lipid residues.

HEFA has enabled the first significant wave of commercial production, but its success has created a concentrated exposure to a relatively narrow feedstock pool. The same raw materials are sought by renewable diesel, biodiesel, marine fuels, oleochemicals, animal feed and other established industries.

The International Energy Agency previously warned that demand from biodiesel, renewable diesel and biojet producers for vegetable oils, waste oils and residue fats could increase by 56%, reaching approximately 79 million tonnes over the 2022–2027 period.

This is not merely a question of physical availability. It is also a question of price.

National Renewable Energy Laboratory assessments show that feedstock is generally the largest cost component in HEFA production. Depending on the oil and project configuration, research has estimated that the feedstock may represent approximately 54% to 82% of the resulting fuel cost.

That changes how SAF competitiveness should be understood. A project may have excellent conversion technology and an efficient refinery, yet remain uncompetitive if it lacks privileged access to stable and affordable raw materials.

As the most attractive waste oils are contracted, procurement may progressively require:

- longer sourcing distances;

- larger numbers of suppliers;

- more complex collection systems;

- increased reliance on imports;

- greater working capital;

- stronger fraud prevention;

- and exposure to changing feedstock eligibility rules.

HEFA will remain essential, but limited oils and fats cannot reasonably supply the entire long-term aviation market. Additional pathways and a much broader feedstock base will be required.

Residues are abundant on paper but difficult in practice

Agricultural and forestry residues appear to offer enormous potential. Straw, maize residues, rice straw, sugarcane trash, bagasse, forestry residues and sawmill by-products are generated in very large quantities.

Yet headline production statistics frequently overstate what an industrial plant can actually procure.

A regional assessment might identify one million tonnes of cereal straw. That figure must subsequently be reduced to account for:

- the material needed to protect soils from erosion;

- the contribution of residues to soil organic carbon;

- existing animal feed and bedding demand;

- technical collection losses;

- fields that cannot be economically accessed;

- moisture and contamination;

- machinery and contractor availability;

- farmer participation;

- storage losses;

- transport distance;

- and year-to-year yield variability.

Only after these deductions can a project estimate the volume that is sustainably removable. A further reduction may then be necessary to determine how much can be commercially contracted and delivered within the plant’s required quality specifications.

This produces four very different figures:

- Residues generated

- Residues sustainably removable

- Residues commercially accessible

- Residues contractable and deliverable

Only the fourth category can operate a refinery.

The same problem arises in forestry. Regional inventories may show substantial woody biomass, but much of it may be distributed across difficult terrain, contain excessive moisture or already supply pulp, panels, pellets, heat, animal bedding and other markets.

Sawmill residues are easier to aggregate, although they are rarely uncommitted. Harvesting residues may be more abundant, but their collection cost, bulk density and moisture can limit the economic sourcing radius.

Therefore:

A resource map is not a supply chain.

The relevant measure is not the total number of tonnes theoretically present in a region. It is the quantity that can be sustainably removed, certified, contracted and delivered to specification throughout the operating life of the plant.

Feedstock reliability must be designed, not assumed

Refineries are designed for continuous operation. Agricultural and forestry systems are not.

Harvests are seasonal. Yields vary with rainfall and temperature. Collection can be interrupted by wet conditions. Farmers change rotations. Forest harvesting responds to wider product markets. Competing buyers appear. Regulations and sustainability classifications evolve.

A bankable supply chain must convert these biological and commercial uncertainties into a predictable industrial input.

That usually requires a portfolio rather than dependence on one resource or supplier. A robust procurement system can combine:

- long-term agreements with anchor suppliers;

- multiple feedstock categories where technically possible;

- geographic diversification;

- owned or controlled production;

- contracted grower networks;

- residue aggregation agreements;

- strategic inventories;

- decentralised storage or preprocessing hubs;

- backup supply corridors;

- clear quality protocols;

- and digital traceability from origin to plant.

This approach is similar to redundancy elsewhere in industrial design. A refinery is not engineered around one critical pump without a contingency. Feedstock, which is often its largest operating cost and one of its largest sources of risk, should not be treated differently.

Feedstock reliability is engineered, not assumed.

Logistics define the real supply basin

Biomass resources are frequently bulky, seasonal and geographically dispersed. Their economic value at the plant gate can be very different from their value at the farm, plantation or forest.

Moisture reduces useful payload. Low bulk density increases the number of truck movements. Poor rural roads restrict seasonal access. Repeated handling introduces dry-matter losses and contamination. Storage adds capital costs, insurance requirements and fire risks.

The economically accessible feedstock basin is therefore determined by logistics as much as by biological availability.

Large centralised plants may capture economies of scale in conversion, but they also require larger sourcing areas. As the collection radius expands, average transport distances and competition with other users usually increase.

Several configurations can address this problem:

Direct delivery works where feedstocks are concentrated and suppliers can meet plant specifications.

Regional aggregation hubs can receive, inspect, blend, dry, chip, bale or store material before onward transport.

Decentralised preprocessing can transform low-density biomass into pellets, torrefied material, pyrolysis liquids, alcohols or other transportable intermediates closer to the resource.

Multimodal logistics can connect road collection with rail, barge or port infrastructure, although each additional transfer creates cost, handling and contractual interfaces.

The optimal model depends on resource density, moisture, road infrastructure, plant scale, technology tolerance and alternative markets. It should be established before finalising plant capacity—not after the refinery has been designed.

Plantations and purpose-grown crops belong in the discussion

The SAF debate often presents feedstocks as a binary choice between desirable wastes and undesirable crops. The real picture is more complex.

Expansion of conventional food crops into forests, wetlands or productive agricultural areas can create serious environmental and land-use risks. However, not all purpose-grown feedstock systems have the same characteristics.

Potential options include:

- perennial lignocellulosic grasses on suitable underutilised land;

- short-rotation woody crops;

- winter oilseeds integrated into existing rotations;

- cover and intermediate crops that do not replace the main harvest;

- agroforestry systems;

- crops adapted to saline, drought-prone or otherwise constrained land;

- and industrial crops established as part of land-restoration programmes.

Dedicated crops require establishment, agronomic management and careful sustainability assessment. But they also provide something that spot-market residues often cannot: a degree of planned supply.

Species, varieties, planting areas, harvesting calendars and production protocols can be selected against a defined industrial requirement. Yields can be monitored and improved. Grower programmes can be expanded progressively. Storage and logistics can be designed around known harvesting periods.

This does not mean that plantations should replace residues. The most resilient projects are likely to develop hybrid portfolios combining:

- industrial by-products;

- sustainably removable residues;

- contracted agricultural production;

- dedicated perennial or woody crops;

- and alternative feedstocks available during supply disruptions.

The Next Feedstock Will Be Grown

Waste and residue streams will remain essential, but they cannot supply unlimited volumes. Future SAF growth will also require purpose-grown feedstocks, intermediate crops and perennial systems developed around reliable industrial demand.

Residues may offer lower establishment costs but limited control. Dedicated crops require earlier investment but can provide greater visibility over future volumes.

The correct balance is project- and region-specific.

Sustainability data have become part of the physical product

SAF is not valued solely by the number of tonnes delivered. Its regulatory and commercial value depends heavily on verified lifecycle greenhouse gas performance.

Two physically similar feedstocks can generate very different emissions reductions depending on:

- land-use history;

- crop and residue management;

- fertiliser use;

- irrigation;

- harvesting energy;

- transport distance;

- processing energy;

- methane avoidance;

- carbon stored or lost in soils;

- and the applicable certification methodology.

The Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA), and regulatory systems in markets such as the European Union impose detailed sustainability and chain-of-custody requirements.

A material that cannot be properly documented may therefore be commercially unusable, even when it is physically suitable for conversion.

Feedstock procurement must capture data at origin. For agricultural materials, this may include field boundaries, previous land use, yields, fertiliser applications, irrigation, fuel consumption, residue-removal practices and transport distances.

For wastes and residues, reliable proof of origin and waste status is essential. High policy premiums can create incentives for misclassification, double counting or substitution with non-eligible materials.

Traceability, sustainability certification and measurement, reporting and verification—commonly called MRV—are not administrative additions to the supply chain. They are part of the product being purchased.

What a bankable SAF supply chain looks like

The next generation of projects will need to demonstrate more than theoretical biomass availability.

Investors, lenders and developers should be able to determine:

- how much feedstock is genuinely available after existing uses;

- how availability changes in a poor harvest year;

- whether residue-removal rates are agronomically sustainable;

- how many suppliers are required;

- which party finances harvesting and storage equipment;

- what proportion of supply is contracted or exposed to spot markets;

- how prices are indexed;

- whether substitute materials can be processed;

- how sustainability and carbon data are verified;

- and what contingency volumes exist.

Long-term procurement agreements may also need to finance or support upstream infrastructure. Farmers and suppliers cannot always guarantee industrial volumes without investment in planting material, harvesting machinery, irrigation, storage, preprocessing or working capital.

These assets should not be considered peripheral to the refinery. They are components of the productive system that enables it to operate.

A strong project will therefore align three development pipelines:

- The conversion pipeline: technology, engineering, construction and commissioning.

- The feedstock pipeline: resource development, agronomy, contracting, certification and expansion.

- The infrastructure pipeline: collection, storage, preprocessing, transport, blending and distribution.

If one advances significantly faster than the others, the project remains exposed.

The real SAF bottleneck is upstream

IATA is right to describe current SAF volumes as disappointing. More effective incentives, realistic mandates, renewable energy and open infrastructure will all be necessary.

But policy cannot automatically create mature feedstock basins.

These must be developed years before a plant begins operation. The work includes land and resource assessment, field-level agronomy, supplier engagement, residue mobilisation, plantation establishment, logistics design, quality control, sustainability certification and long-term contracting.

The successful SAF projects of the next decade will not necessarily be those with the largest theoretical resource maps or the most ambitious production announcements.

They will be those capable of transforming biological resources into reliable, traceable and financeable industrial supply.

SAF growth is not yet SAF scale. And SAF will not reach scale without reliable feedstock.

Developing reliable SAF feedstock supply chains

Bioenergy Crops supports sustainable aviation fuel developers, investors, technology providers and industrial partners in the assessment and development of long-term feedstock strategies.

Our work covers biomass resource assessment, agronomic development, agricultural and forestry residues, dedicated crop systems, procurement models, logistics, sustainability, Measurement, Reporting and Verification (MRV), and long-term supply-chain implementation.

Contact Bioenergy Crops to discuss the feedstock requirements of your SAF project.

References

- International Air Transport Association, SAF Production Volumes Still Disappointing, June 2026.

- International Air Transport Association, Quarterly Air Transport Chartbook, first quarter 2026.

- International Energy Agency, Renewables 2025: Renewable Transport.

- International Energy Agency, Is the Biofuel Industry Approaching a Feedstock Crunch?

- International Energy Agency, Biofuels: Tracking Clean Energy Progress.

- International Civil Aviation Organization, Sustainable Aviation Fuels Guide.

- International Civil Aviation Organization, CORSIA Eligible Fuels and Sustainability Criteria.

- Calderón, O’Neill and Rodríguez, National Renewable Energy Laboratory, Sustainable Aviation Fuel State-of-Industry Report: Overall State of the Industry and Feedstock Assessment, 2024.

- Moriarty and Kvien, National Renewable Energy Laboratory, Sustainable Aviation Fuel Blending and Logistics, 2024.

- Wiatrowski and co-authors, Algae to HEFA: Economics and Potential Deployment in the United States, Biofuels, Bioproducts and Biorefining, 2024.

- US Department of Energy, Sustainable Aviation Fuel Grand Challenge Roadmap and Implementation Framework.

Related BEC reading: Camelina and carinata for SAF feedstock development.