Why regional feedstock basins combining residues, intermediate crops and dedicated energy crops are becoming strategic infrastructure for SAF, renewable fuels and biobased industries.

An energy market can change in days. A reliable feedstock basin is built over seasons and years. That difference is becoming one of the most important constraints in renewable fuels and biobased industry.

When oil prices move, refining margins change immediately. When aviation policy accelerates, airlines and fuel suppliers can sign offtake agreements quickly. When a government raises a blending mandate, the signal can be issued in a press release. Feedstock, however, does not respond at the same speed. It has to be found, grown, harvested, collected, stored, tested, certified, transported and delivered. It has to fit a farm business before it can support an industrial balance sheet.

That is why the next generation of renewable-fuel and biobased industrial projects will increasingly be built around geographically connected, diversified and traceable feedstock basins. A feedstock basin is a geographically connected production and sourcing area capable of supplying defined industrial demand through a coordinated combination of crops, residues, infrastructure, contracts and traceable logistics.

This is a different proposition from a biomass map, a crop suitability study or a list of potential suppliers. A feedstock basin links land, residues, growers, storage, processing, logistics, sustainability certification, carbon accounting and long-term offtake into a system that can be financed and repeated.

Energy supply chains are moving upstream

Renewable-fuel developers, refiners and offtakers are being pulled upstream into questions that used to sit mainly with agriculture, forestry and commodity origination teams. They need to know whether a region can supply annual volumes, whether the feedstock will meet specification, how far it can be transported, how it stores, who controls it, which alternative markets already compete for it and whether the carbon and sustainability claims can be documented.

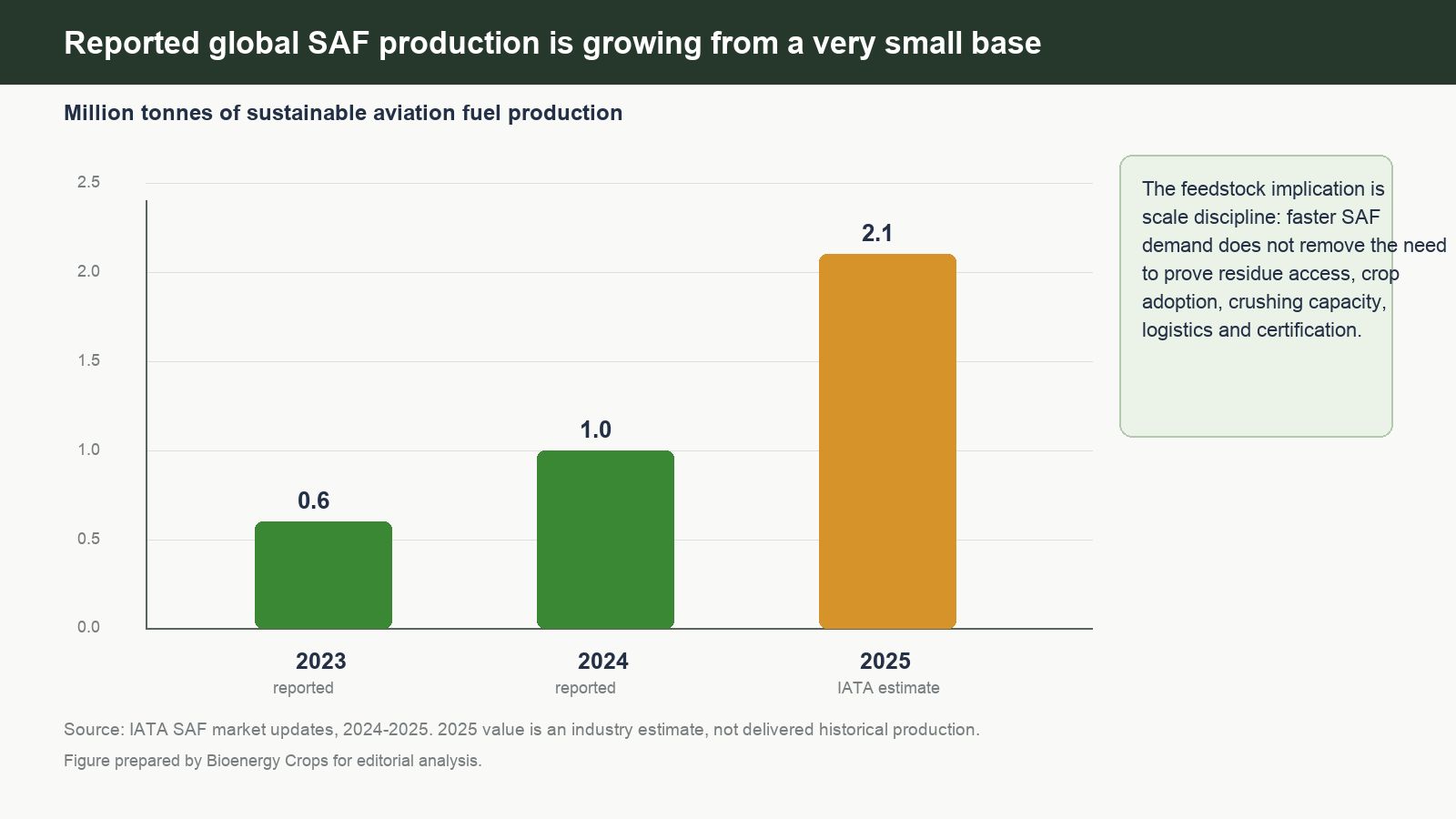

That upstream movement is visible across sustainable aviation fuel (SAF), hydrotreated vegetable oil (HVO), biomethane, biochar, bio-based chemicals and advanced fuels. Refinery technology matters, but the industrial asset is exposed if the feedstock system remains immature. A project may be technically attractive and still be difficult to finance if the resource is only theoretical, if collection costs are weakly evidenced, or if grower participation has not moved beyond expressions of interest.

For investors and project-finance teams, this changes the due-diligence question. The issue is no longer only whether a crop can grow or whether residues exist. It is whether the project can control enough specification-compliant feedstock at a delivered cost that supports debt service, carbon claims and industrial uptime. For growers, the question is equally practical: does the new crop or residue contract improve the whole farm rotation after seed, fertiliser, crop protection, machinery, drying, delivery, risk and payment timing are considered?

Bayer and camelina are a signal of a wider transition

A recent Reuters report on Bayer and bp’s newgold platform is useful because it shows how far upstream energy-market strategy is moving. The report described Bayer and bp developing camelina and related intermediate oilseed supply, with Bayer contributing genetics, seed technology, agronomy and farmer access, and bp contributing renewable-fuel demand, energy-market access and industrial conversion. The reported context was not that the concept began with the latest geopolitical disruption, but that energy-security concerns associated with the Iran conflict increased interest in accelerating regional supply options.

The important point is not simply that camelina can be grown. It is that the commercial platform has to connect breeding, seed multiplication, grower recruitment, agronomic support, contracting, crushing, oil logistics, traceability, carbon intensity and offtake. Announced acreage targets are therefore not the same as planted hectares, harvested production or delivered oil. They are signals of intended scale, which must be converted into verifiable agricultural and industrial execution.

Camelina is attractive because it can fit some intermediate-crop windows, can produce oil for renewable diesel or SAF pathways, and may offer a shorter development cycle than some perennial feedstocks. It also carries agronomic and commercial risk. Establishment, seed size, weed management, harvest timing, yield stability, local crushing capacity and farmer economics all matter. Intermediate-crop status and low-carbon eligibility depend on the production system and regulatory framework, not on the crop name alone.

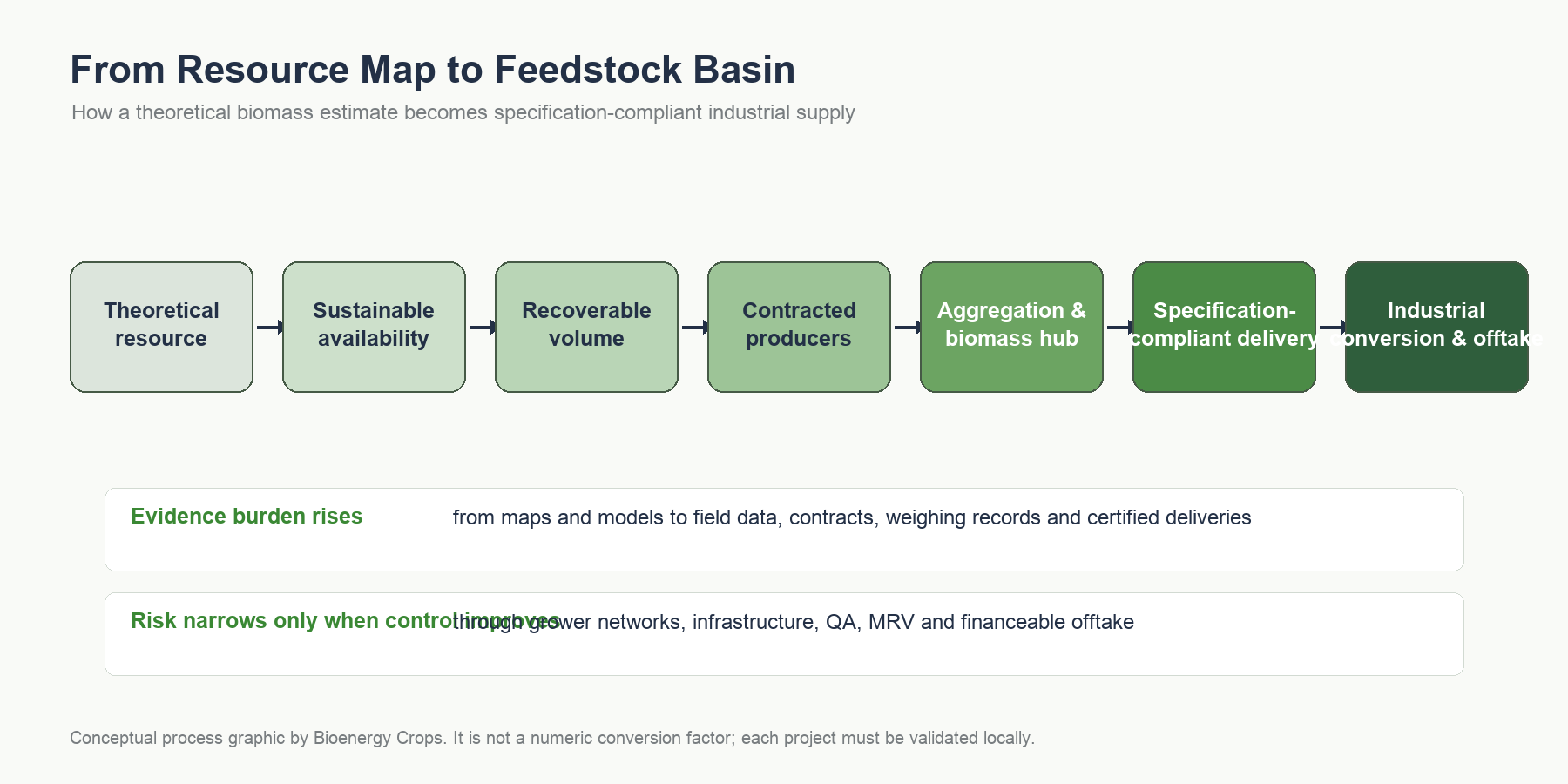

From biomass availability to feedstock basins

The gap between availability and supply is where many bioenergy projects become weaker than they appear in early presentations. A theoretical resource describes what may exist in a region. A technically available resource removes material that cannot realistically be accessed. Sustainable availability adds land-use, biodiversity, soil, water, social and regulatory constraints. Recoverable supply includes machinery, roads, storage, seasonal windows and operational losses. Commercially accessible supply reflects competing uses, price expectations and supplier willingness. Contracted supply proves legal access. Specification-compliant delivered supply is the quantity that actually reaches the industrial plant at the required quality, moisture, contamination level, traceability and delivery schedule.

A million tonnes on a biomass map are not a million tonnes delivered to a plant.

This progression matters for finance because each step changes risk. Banks and infrastructure investors do not lend against theoretical biomass. They lend against credible access, cost, contracts, logistics, technical performance and downside cases. Offtakers need continuity, not merely optionality. Carbon and ESG teams need documented land-use status, carbon intensity, monitoring, reporting and verification (MRV), and clear rules for additionality and farmer participation.

| Category | Meaning | Evidence required | Investor relevance | Typical uncertainty |

|---|---|---|---|---|

| Theoretical resource | Material estimated to exist in a region. | Land cover, crop statistics, forestry or residue datasets. | Useful for screening only. | High. |

| Sustainable availability | Resource remaining after environmental, social and regulatory filters. | Land-use, biodiversity, soil, water and tenure review. | Reduces reputational and permitting risk. | Medium to high. |

| Recoverable supply | Material that can be collected within practical machinery, season and access limits. | Field operations, roads, storage, yield and loss assumptions. | Tests operational feasibility. | Medium. |

| Contractable supply | Resource that suppliers are willing to commit under acceptable terms. | Grower and supplier agreements, price mechanisms and risk sharing. | Supports bankability. | Medium. |

| Delivered feedstock | Specification-compliant material arriving at the plant. | Weighbridge data, QA, chain of custody, certification and delivery records. | Highest relevance to lenders and offtakers. | Lower, if proven over time. |

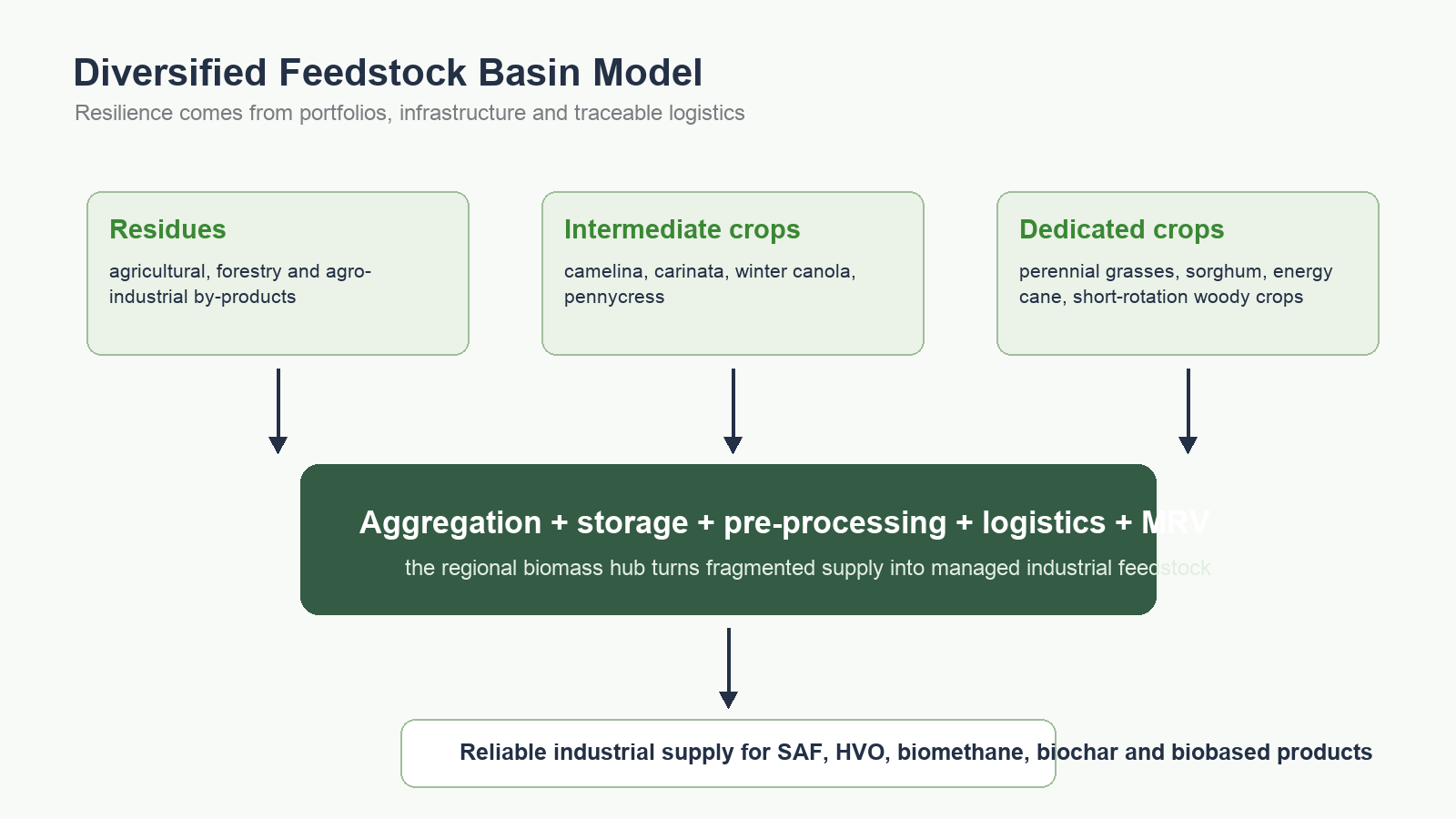

Why diversified feedstock basins are more resilient

Resilient basins rarely depend on a single source of biomass. They combine feedstocks with different seasons, risk profiles, storage characteristics and market roles. That does not mean indiscriminate mixing. Each feedstock has to match an industrial route, a specification and a realistic delivered-cost model.

Existing agricultural, forestry and agro-industrial residues

Residues can offer relatively fast mobilisation where supply chains already exist. Straw, pruning residues, forestry residues, mill by-products and food-processing streams may support biomass heat, biochar, biomethane, advanced fuels or pre-processing hubs. Their limits are also clear: competing uses, nutrient removal, soil cover needs, contamination, moisture, seasonality, transport density and ownership can all reduce the accessible volume. Residues should be assessed as managed resources, not as waste waiting to be taken.

Intermediate crops within existing rotations

Intermediate oilseeds such as camelina and carinata, as well as winter canola and pennycress in selected systems, can add oil supply without requiring a permanent land-use change where they fit genuine rotation windows. Their value depends on agronomy and whole-rotation economics. A grower will judge seed cost, nitrogen and sulphur requirements, machinery, weed risk, water use, harvest timing and effects on the following crop. For refiners, the questions are oil quality, crushing access, traceability and consistency of volumes.

Dedicated energy crops for predictable supply

Perennial grasses, biomass sorghum, energy cane, short-rotation woody crops and dedicated oil-bearing systems such as macaúba can provide more predictable feedstock once established. They may be relevant for lower-productivity land, erosion-prone areas, degraded land or integrated farming systems, but they require disciplined site assessment. Establishment cost, time to maturity, harvest systems, long-term contracts and land tenure become central. Dedicated crops can improve supply reliability only when they are developed with growers and landowners over a realistic horizon.

Energy resilience will increasingly come from regionally diversified feedstock portfolios.

Marginal land requires disciplined assessment

Marginal land can be strategically important, but it is often discussed too casually. Lower-productivity land is not automatically vacant, available or environmentally suitable. It may support grazing, biodiversity, water regulation, cultural values, carbon stocks or informal uses that are not visible in a simple suitability map.

A credible marginal-land bioenergy strategy evaluates soil capability, rainfall, climate risk, slope, erosion, access, existing land use, ownership, tenure, biodiversity, above-ground and below-ground carbon, social considerations, additionality, long-term productivity and distance to processing. It also tests whether the proposed crop can survive and produce economically without transferring unacceptable risk to the farmer or landowner.

This is why replicability comes from the sourcing and development model, rather than from planting the same crop everywhere. The same methodology can be applied in the Northern Great Plains, the Canadian Prairies, Argentina and the Southern Cone, Mediterranean regions, Central and Eastern Europe or selected tropical basins. The crop portfolio, contract structure and hub design will differ.

Biomass hubs are the missing regional infrastructure

Many regions have biomass but lack the infrastructure that turns dispersed supply into industrial feedstock. Biomass hubs can perform collection, weighing, quality control, drying, cleaning, storage, baling, chipping, milling, densification, crushing, blending, pyrolysis, digestion, pre-processing, traceability and dispatch. They can also serve more than one market: renewable fuels, industrial heat, biomethane, biochar, animal bedding, soil amendments or biobased products.

The hub does not remove the need for field-level discipline. It reduces fragmentation. It creates a place where quality is measured, logistics are consolidated, documentation is generated and material can be matched with several industrial routes. For project finance, that can make the difference between a collection concept and a managed supply chain.

The next competition will be for feedstock origination capacity

Feedstock origination is becoming a strategic capability. It involves identifying resources, securing grower and supplier participation, developing agronomy, contracting volumes, organising storage and logistics, controlling quality, documenting sustainability and delivering data for carbon accounting. It is not the same as buying spot biomass after a plant has been built.

The next competitive advantage will be feedstock origination capacity.

Originators that can build trusted relationships with growers, cooperatives, landowners, forestry operators, traders and processors will shape which projects become bankable. They will also influence price formation, supplier retention and barriers to entry. A refinery with several theoretical feedstock options may still be weak if another actor has already secured the region’s practical supply base.

Argentina and the emergence of commercial camelina basins

Argentina is a useful example of an emerging camelina basin because it combines extensive agricultural production, technically experienced growers, established machinery and contracting, potential rotation windows, crushing capacity and export infrastructure. Its relevance may extend into Uruguay and Paraguay where agronomy, logistics and processing can be coordinated across the Southern Cone.

The public evidence should be read carefully. Agroclimatic potential, field trials, planted area, contracted area, harvested production, delivered seed, crushed oil and industrial fuel production are different categories. Some commercial programmes report targets, grower recruitment or development intentions, while comparable public figures for harvested hectares, delivered tonnes and crushed oil are often incomplete. That lack of comparable public data is itself important for investors: it shows why feedstock maturity cannot be inferred from regional suitability alone.

The Southern Cone should therefore be treated as a promising development arena rather than a fully proven industrial supply base. Its strengths are real, but commercial maturity depends on repeated campaigns, contract performance, crushing economics, logistics, certification and delivered oil cost. The same discipline applies to camelina and carinata development in North America, Canada, Central and Eastern Europe and Mediterranean regions.

Replicability comes from the development model

A replicable feedstock-basin model starts with industrial demand and specifications, then establishes the economic sourcing radius. It maps land, residues, crops, infrastructure and existing uses. It separates theoretical, sustainable, recoverable and contractable supply. It selects a diversified feedstock portfolio, conducts local trials and validation, builds grower and supplier networks, designs collection and storage, develops contracts, implements MRV and certification, and scales supply in line with industrial commissioning.

This sequence can be adapted to several industrial routes. A region may supply SAF lipids, biomass heat, biomethane, biochar and biobased products from different fractions of the same basin. The development model is what travels: disciplined assessment, phased validation, supplier development, infrastructure, contracts and traceability.

Replicability comes from the sourcing model, rather than from planting the same crop everywhere.

| Feedstock type | Examples | Principal advantage | Main constraint | Typical role |

|---|---|---|---|---|

| Residues | Straw, forestry residues, pruning residues, agro-industrial by-products. | Can mobilise existing material. | Competing uses, quality, collection cost and sustainability limits. | Early volume and flexibility. |

| Intermediate crops | Camelina, carinata, winter canola, pennycress. | Can fit rotation windows where agronomy allows. | Farmer economics, yield risk, crushing and certification. | Oilseed supply and rotation diversification. |

| Dedicated energy crops | Perennial grasses, biomass sorghum, energy cane, short-rotation woody crops, macaúba. | Potentially more predictable long-term supply. | Establishment time, land tenure, contracts and harvest systems. | Strategic base-load feedstock. |

What investors, industrial developers and offtakers should examine

Due diligence should begin with resource maturity. Is the feedstock theoretical, sustainable, recoverable, contracted or already delivered? Which competing uses exist? What is the collection radius at a delivered cost the project can tolerate? How seasonal is the feedstock, and what storage is required? Which quality parameters matter for the conversion technology?

Industrial developers should test substitution between feedstocks, pre-processing needs, moisture tolerance, contamination risk, crushing or densification access, and dispatch reliability. Offtakers should review continuity, chain of custody, certification, regional diversification and price formation. Carbon and ESG teams should review land-use change, biodiversity, water, soil carbon, additionality, farmer participation, social risk and tenure.

Growers and landowners need the same transparency from the other side. They need to understand net margin, crop-failure risk, seed availability, fertiliser and crop-protection needs, machinery, water use, harvest logistics, delivery requirements, payment timing, contract terms and implications for the following crop. A feedstock basin that does not work for producers will not be reliable for refiners.

Conclusion: energy security begins before the refinery

The next energy supply chain will be built before the refinery gate. It will be built through land assessment, growers, contracts, biomass hubs, traceability and the capacity to deliver sustainable feedstock year after year.

That does not mean every region should grow the same crop, or that every biomass resource should be pushed into fuel. It means that renewable-fuel and biobased industrial projects need a sourcing model with enough agronomic, logistical, financial and sustainability evidence to be repeated responsibly. The regions that can organise residues, intermediate crops, dedicated energy crops, lower-productivity land, biomass hubs and MRV into coherent basins will have a strategic advantage.

Bioenergy Crops supports developers, investors, industrial partners and offtakers with feedstock resource assessment, GIS, crop and land evaluation, residue mapping, field validation, grower development, logistics, delivered-cost modelling, sustainability, MRV and feedstock supply-chain design.

Selected sources and further reading

- Reuters, “Bayer hopes to speed up biofuel feedstock plan amid Iran war energy crunch”, 2026.

- IATA, Disappointingly slow growth in SAF production.

- Regulation (EU) 2023/2405 on ensuring a level playing field for sustainable air transport.

- Bioenergy Crops: Feedstock Resources & Supply Chains.

- SAF Will Not Scale Without Reliable Feedstock.

- Camelina and Carinata for SAF.

- Macaúba and dedicated SAF feedstock development in Brazil.

- Energy crops for marginal lands.